Why Estimated Tax Payments Matter – For Small Business Owners, Freelancers, Consultants, and Even W-2 Employees

Taxes are not meant to be paid all at once at the end of the year.

The core principle of the tax system is pay-as-you-go—taxes are paid as income is earned.

This principle is enforced through automatic tax withholding on wages, as well as estimated tax payments for self-employed and other non-withheld income.

Many people believe estimated taxes apply only to small business owners, freelancers, or consultants. In reality, even W-2 employees may be required to make estimated tax payments under certain circumstances.

Understanding this concept early can prevent unpleasant surprises at tax time.

What Are Estimated Tax Payments?

Estimated taxes are quarterly payments made to the IRS and often to state tax agencies for income that is not subject to automatic withholding, such as payroll withholding.

In simple terms, the IRS expects you to:

“Pay taxes as you earn income, not all at once when you file your return.”

Income That Commonly Requires Estimated Taxes

You should consider estimated tax payments if you receive any of the following types of income:

Business income reported on Schedule C

Freelance income reported on Form 1099-NEC

Consulting income

Rental income

Interest and dividend income

Large capital gains from stocks, cryptocurrency, or real estate

Pass-through income from S corporations or partnerships

A simple rule of thumb:

If no tax is automatically withheld, estimated taxes are likely required.

Why Estimated Taxes Are Important

Failing to make estimated tax payments on time can result in:

A large lump-sum tax bill at filing time

IRS underpayment penalties

Cash-flow strain and financial stress

A common misconception is:

“I paid everything when I filed my return, so I should be fine.”

Unfortunately, that is not how the IRS evaluates compliance.

The IRS considers both the amount paid and the timing of payment.

Paying all taxes at once in April does not automatically eliminate underpayment penalties.

Real-Life Examples (2025 Tax Year)

Example 1: Freelance Designer

In 2025, a freelance designer earned:

Total 1099-NEC income

$120,000

Business expenses

$30,000

Net profit

$90,000

This income is subject to:

Self-Employment Tax at 15.3 percent

(12.4 percent Social Security + 2.9 percent Medicare)

Self-employment tax is calculated as:

Net profit × 92.35 percent × 15.3 percent

$90,000 × 92.35% × 15.3% ≈ $12,700

After adding federal income tax, total tax liability exceeded $25,000.

Because no estimated tax payments were made during the year, the taxpayer was required to pay the full amount in April 2026, plus IRS underpayment penalties.

Lesson: Steady income does not guarantee tax readiness.

Example 2: First-Year Independent Consultant

A consultant left a salaried job mid-year and earned:

W-2 wages (first half of the year)

$60,000

Consulting net income (second half)

$80,000

Although taxes were withheld from wages, no tax was withheld from consulting income.

Self-employment tax alone:

$80,000 × 92.35% × 15.3% ≈ $11,300

Federal income tax was added on top of this amount.

Lesson: Having W-2 wages does not eliminate estimated tax obligations for business income.

Example 3: W-2 Employee With Large Capital Gains

A full-time employee had proper payroll withholding throughout 2025.

In September, long-held stock was sold, generating:

Capital gain

$150,000

Employer withholding does not account for capital gains.

Because no estimated tax payment was made, the taxpayer faced:

Significant capital gains tax

IRS underpayment penalties

Lesson: Even W-2 employees may need estimated tax payments when large capital gains occur.

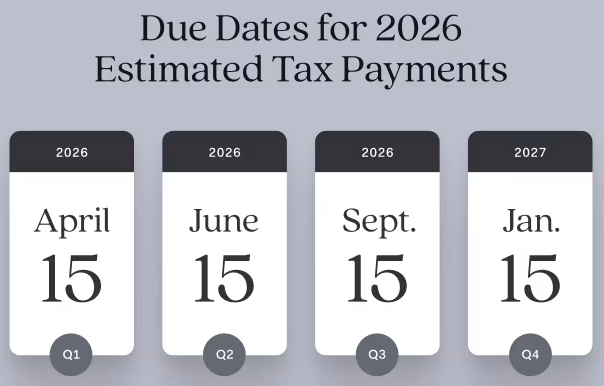

Estimated Tax Due Dates for 2025

Estimated taxes are generally paid quarterly:

April 15

June 15

September 15

January 15 of the following year

If a due date falls on a weekend or federal holiday, the deadline moves to the next business day.

Practical Ways to Manage Estimated Taxes

Use IRS safe harbor rules based on prior-year tax liability

Set aside a portion of income in a dedicated tax savings account

Review income and tax projections quarterly

Increase withholding on W-2 wages using Form W-4 as an alternative

From a practical standpoint, many self-employed taxpayers find it prudent to reserve 25 percent to 30 percent of net income for taxes.

This is a planning guideline based on experience, not an IRS rule.

Final Thoughts

Estimated taxes are not a penalty system.

They are a pay-as-you-go tax mechanism built into the U.S. tax system.

For small business owners, freelancers, and consultants, estimated tax planning is not optional—it is a core financial habit.

And while often overlooked, W-2 employees can also be subject to estimated taxes depending on their situation.

Understanding this early can significantly reduce tax surprises and year-end stress.

Note: This article is intended for informational purposes only and does not constitute tax advice. For personalized guidance, please consult a tax professional.